Dear Trade Finance Firms – The FCA Wants You To Do More :

The recent Dear CEO letter shared by the FCA & PRA has sent a stern warning to businesses operating in trade finance – more needs to be done.

The letter was addressed directly to the CEOs of firms carrying out trade finance business and has caught the full attention of the industry due to its direct nature. It outlines a clear need for change but includes a marked shift in tone from traditionally sanitary messages of “advice” or guidance, instead laying out staunch requests for businesses to improve their oversight of their current position.

After a number of significant, high profile losses within the commodity trading industry in recent years, trade finance and credit risk analysis has hardly ever been in the spotlight so often.

The position of the FCA & PRA is made clear from the start, their hands have been forced to respond after overwhelming recent evidence pointed to insufficient due diligence.

“Our recent assessments of individual firms have highlighted several significant issues relating to both credit risk analysis and financial crime controls. These issues have exposed firms to unnecessary risks that are material in both a conduct and prudential context.”

In response to this, they are demanding more from firms when it comes to risk assessment, counterparty analysis and transaction monitoring.

Reacting to an uncertain market

The letter addresses the uncertainty of the market and the prolonged, increased opportunities for fraud and non-compliance. They make clear that the existing framework adopted by many firms is not fit for purpose, especially in this changeable market.

A post-pandemic wave of financial crime has been threatened for some time, with KPMG forecasting that a tsunami of fraud was en route in 2021 and beyond. While the warnings have been public and plain to see, it’s surprising that firms aren’t already embracing additional risk management considering the uncertainty we all currently face.

The letter highlights the “focus and assessment of financial crime risk factors” as just one of the insufficiencies commonly displayed in recent assessments. Others include poorly evidenced decision making, notably when it comes to residual risk.

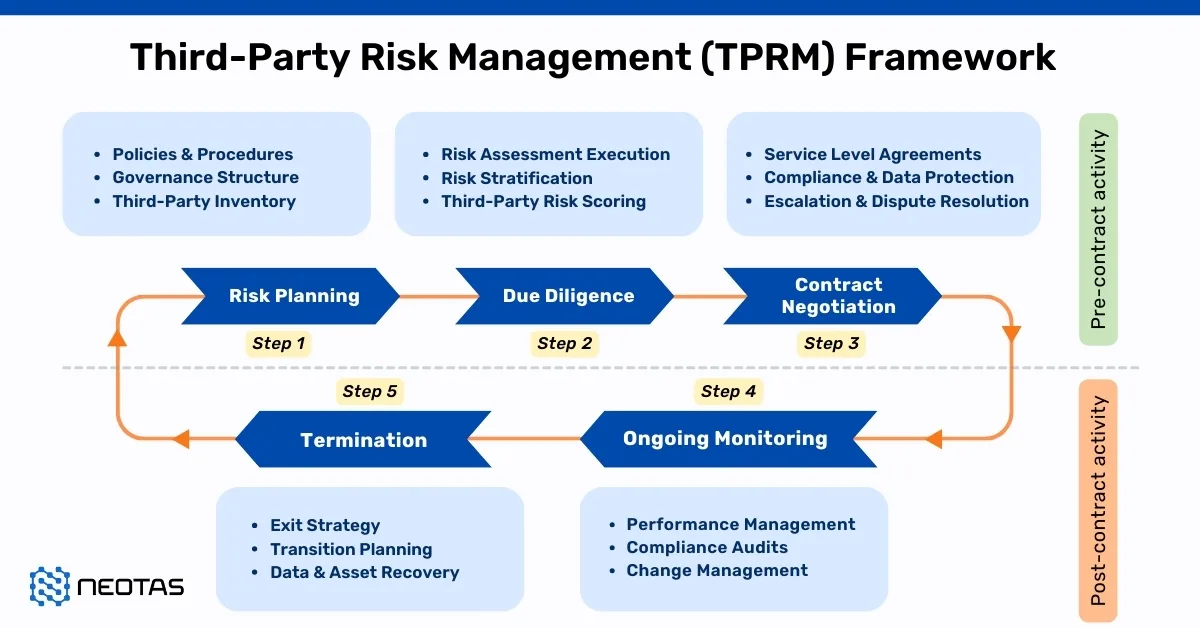

The Right Tool For The Job

There is a warning of how failing to properly address risks can lead to exposure to financial crime, to non-compliance, to suspicious activity and to the consequences that may come as a result.

The expectation continues to be that some deals inherently require a greater degree of diligence than others, on both sides of the transaction. It is the duty of the transacting firms to comply with the expected levels of diligence required.

Amongst the tools suggested in the letter, there is an explicit directive to consider where enhanced due diligence and non-financial risk evaluation should be required. Many of the “red flags” listed in the letter including money laundering, adverse media and more are typically discovered as part of open source EDD, like we provide at Neotas.

We wrote previously of how non-financial risk identification could be the difference maker when it comes to credit risk and the same principles apply across the industry.

As counterparty networks become ever-more complex, the importance of full network analysis is highlighted in the letter with a clear directive that all parties related to a transaction should be appropriately considered.

Network analysis remains at the core of many of our investigations, particularly for clients working in trade finance. In these cases the front-facing counterparty often displays little to be concerned about, only to find risks hidden within their network.

Discoveries of networks including undisclosed PEPs, directors and relationships are common – a recent case also uncovered terrorist financing linked to a seemingly “clean” subject. Without diving into the network of the counterparty, you cannot fully understand the risks.

An Example: Network Analysis Uncovers Fraudulent Activity

A recent case of enhanced due diligence for Channel Capital uncovered a host of suspicious behaviours associated with the network of a subject in a European company.

While reviewing the company and its director, full network analysis uncovered evidence linking the subject to a number of bankrupted companies.

Uncovering the details of the bankrupted businesses allowed us to discover suspicious payments made between the European company and the newly discovered entities. Payments that were being made in an effort to manipulate the subject company’s books in order to appeal to investors.

The insights uncovered informed Channel’s decision making, who eventually halted the deal and alerted the authorities of the fraudulent payments.

Download the full case study here

Not-knowing is not good enough

While not knowing or being unaware of non-compliance has never been a defensible argument, the tone from the regulators in the letter is stark:

“This letter has reiterated our expectations of firms when undertaking trade finance activity.”

The message could not be clearer and should come as a stern warning. Our discussions with clients often center around the idea that “if the information is out there, wouldn’t you want to know about it?”. The message from the FCA and PRA seems to have shifted to a more definitive:

“If the information is out there, you should know about it”.

Supplementing Existing Guidance

“The expectations set out in this letter are not exhaustive and should be considered alongside relevant rules and guidance such as Joint Money Laundering Steering Group guidance, the PRA Rulebook and the FCA’s Financial Crime Guide.”

While it’s made clear that the new recommendations aren’t exhaustive, the instruction here is to apply additional scrutiny to transactions, particularly when there is a need for a deeper dive.

Firms have been instructed to be reactive and responsible for the deals they are a part of, evidencing transparent, informed decision-making along the way.

A gauntlet has been laid down by the regulators in no uncertain terms. Firms should continue to apply traditional due diligence while embracing new technologies, such as EDD, to help protect all parties and maintain compliance. It will be interesting to see who rises to the challenge.

Trade Finance Firms :

Trade finance firms are essential entities in global commerce, serving as financial intermediaries that facilitate international trade transactions. They offer a spectrum of services and instruments vital for businesses engaging in cross-border trade. These services encompass letters of credit, supply chain financing, export and import financing, trade credit insurance, and documentary collections. Trade finance firms also specialize in compliance, risk management, and trade advisory services, helping clients navigate complex regulations and manage trade-related risks effectively. Their expertise and support enable businesses to optimize cash flow, mitigate risks, and ensure the smooth flow of goods and services across borders, fostering economic growth and international business expansion.