Anti-Money Laundering (AML)

Anti-Money Laundering (AML) is a comprehensive framework of policies, regulations, and procedures established to prevent individuals and entities from disguising illegally obtained funds as legitimate income within the financial system. Its primary purpose is to detect and deter financial crimes by tracing and halting the flow of funds originating from illicit activities. AML serves as a crucial safeguard for the integrity and stability of the financial sector.

Money laundering, the primary target of AML, encompasses various illegal activities, including drug trafficking, tax evasion, bribery, corruption, and financing of terrorism. The core objective of AML is to identify and disrupt these unlawful financial transactions, making it challenging for criminals to enjoy the proceeds of their crimes undetected.

History of AML

The history of AML stretches back several decades and reflects the ongoing battle against financial crime. In the United Kingdom, one significant milestone was the adoption of the Money Laundering Regulations in 1993, which laid the groundwork for combating money laundering within the country. These regulations were followed by further developments, including the Proceeds of Crime Act 2002 (POCA), which provided a more robust legal framework for AML efforts.

Internationally, the Bank Secrecy Act (BSA) of 1970 in the United States marked one of the earliest attempts to address money laundering on a broader scale. Subsequent events, such as the 9/11 terrorist attacks, prompted increased global focus on AML and led to the expansion of AML efforts to encompass counter-terrorism financing (CTF).

In the UK, AML measures have been continually updated and reinforced to keep pace with evolving financial crimes and emerging threats. The Financial Conduct Authority (FCA) and the National Crime Agency (NCA) are among the regulatory bodies overseeing AML compliance in the UK. These agencies work in conjunction with financial institutions and businesses to uphold the nation’s commitment to combating money laundering and safeguarding the financial system’s integrity.

Anti-Money Laundering (AML) is a comprehensive framework aimed at preventing, detecting, and prosecuting money laundering activities. AML measures are crucial for maintaining the integrity of the financial system and are enforced through a combination of policies, regulations, and standards, both at the national and international levels.

Anti-Money Laundering (AML) Policies and Regulations

1. Laws and Legislation

AML laws and legislation serve as the foundation of efforts to combat money laundering. These laws typically require financial institutions and other regulated entities to establish internal controls designed to detect and report suspicious activities. The specific requirements can vary significantly from one jurisdiction to another but generally include the following key components:

- Customer Due Diligence (CDD): Financial institutions must verify the identity of their customers and understand the nature of their customers’ activities. This process helps in assessing the risk level of customers and in monitoring transactions that deviate from the expected pattern.

- Record Keeping: Entities are required to keep detailed records of financial transactions for a specified period. This ensures that there is a trail that can be followed in the event of an investigation into suspicious activities.

- Suspicious Activity Reporting (SAR): Financial institutions must report transactions that they suspect might be related to money laundering to the relevant authorities without notifying the parties involved.

- Compliance Programs: Organisations must develop and implement AML compliance programs, which include policies, procedures, and controls that mitigate the risk of the institution being used for money laundering.

2. Regulatory Authorities

Regulatory authorities are responsible for overseeing the implementation of AML laws and regulations within their jurisdictions. These bodies have the authority to issue guidelines, conduct inspections, and enforce compliance through penalties or other disciplinary actions. Examples include the Financial Conduct Authority (FCA) in the UK, the Financial Crimes Enforcement Network (FinCEN) in the US, and similar bodies in other countries.

3. International Standards (FATF)

The Financial Action Task Force (FATF) is an intergovernmental organisation that sets international standards for combating money laundering, terrorist financing, and other related threats to the integrity of the international financial system. The FATF Recommendations are recognised as the global AML standard and are designed to be implemented by countries in their domestic legislation. Key FATF Recommendations include:

- Implementing effective AML/CFT (Combating the Financing of Terrorism) measures.

- Conducting national risk assessments to understand and mitigate risks.

- Establishing beneficial ownership registries to prevent misuse of legal entities.

- Enhancing international cooperation among countries to combat cross-border financial crimes.

Compliance with FATF Recommendations is assessed through a mutual evaluation process, which examines the adequacy of a country’s AML/CFT laws and the effectiveness of their implementation. Countries that fail to comply with FATF standards may be subject to increased monitoring or be listed as high-risk jurisdictions, which can have significant economic and financial implications.

AML policies and regulations are essential for safeguarding the financial system against the threats posed by money laundering. By adhering to national laws, cooperating with regulatory authorities, and aligning with international standards like those set by the FATF, countries and financial institutions play a crucial role in the global fight against financial crime.

Anti-Money Laundering (AML) encompasses a range of practices and regulations designed to detect and prevent the illicit flow of funds. Understanding key concepts within AML is crucial for effectively combating financial crimes.

Key Concepts in AML

1. Money Laundering

Money laundering is the process of disguising the origins of illegally obtained money, making it appear as if it originated from legitimate sources. The process typically involves three stages:

- Placement: Illicit funds are introduced into the financial system, often through small deposits or purchases to avoid detection.

- Layering: Complex layers of financial transactions are created to obscure the source of the money. This may involve transferring money between different accounts, countries, or entities.

- Integration: The ‘cleaned’ money is reintroduced into the economy as legitimate funds, which can then be used without suspicion.

The aim of money laundering is to enable criminals to enjoy their proceeds without risking detection and prosecution.

2. Predicate Offenses

Predicate offenses are specific criminal acts that generate proceeds, which are then laundered. These underlying crimes can vary widely, including drug trafficking, fraud, corruption, and many other forms of illegal activity. AML regulations target not only the laundering process but also seek to address the proceeds from these predicate offenses, making it critical to identify and curb the initial illegal activities.

3. Terrorist Financing

Terrorist financing refers to the process of providing financial support to individuals or groups engaged in terrorism. Unlike money laundering, which seeks to disguise the origins of money, terrorist financing may involve funds from legitimate sources but aims to conceal the destination or purpose of the money. The primary concern is the use of the financial system to fund activities that pose threats to national and international security.

4. Proliferation Financing

Proliferation financing involves the provision of funds or financial services that contribute to the development and spread of weapons of mass destruction (WMDs) and their delivery systems. This includes financing the trade of goods, services, and technology used in the manufacture of nuclear, chemical, and biological weapons and their delivery mechanisms. Preventing proliferation financing is crucial for maintaining global security and is a key component of international AML and counter-terrorist financing (CFT) efforts.

These concepts are interlinked and form the backbone of AML strategies. Effective AML frameworks are designed to detect and prevent activities related to money laundering, address predicate offenses, and curb the financing of terrorism and proliferation of WMDs. Financial institutions, regulatory bodies, and international organisations must work collaboratively to enforce AML measures, adapt to emerging threats, and safeguard the integrity of the global financial system.

The economic effects of AML (Anti-Money Laundering) crimes are extensive and multifaceted, impacting not just the financial sector but also the broader economy and governance structures. Understanding these impacts is essential for formulating effective countermeasures.

Economic Effects of AML Crimes

1. Threats to Financial Sector

AML crimes undermine the integrity and stability of financial institutions by exposing them to operational, legal, and reputational risks. Money laundering activities can distort asset values and lead to misallocation of resources, eroding trust in financial systems. This can deter investment and lead to inefficiencies in financial markets.

2. Hot Money Flows

Money laundering often involves moving illicit funds across borders, leading to unpredictable “hot money” flows. These flows can cause excessive volatility in exchange rates and interest rates, making economic management more challenging for authorities. Hot money can create bubbles in asset markets and contribute to economic instability when these bubbles burst.

3. Banking Crises

Significant incidents of money laundering within a country’s financial institutions can precipitate banking crises. If banks are seen as compromised, depositors may lose confidence, leading to bank runs. Additionally, fines and sanctions imposed on banks for AML violations can weaken the capital position of these institutions, further destabilising the banking sector.

4. Revenue Collection

AML crimes, particularly tax evasion and fraud, can significantly reduce government revenue. This shortfall limits the government’s ability to invest in public services and infrastructure, affecting overall economic development and the quality of governance.

5. Governance Weaknesses

Money laundering is often linked to corruption and criminal enterprises, which can infiltrate and weaken state institutions. This undermines the rule of law and erodes democratic governance, leading to a vicious cycle where weakened institutions are less able to combat money laundering and associated crimes.

6. Reputational Risks

Countries and financial institutions implicated in AML crimes face severe reputational damage. This can lead to a loss of investor confidence, reduced foreign direct investment, and challenges in accessing international financial markets. For countries, this can translate into higher borrowing costs and reduced economic growth.

7. Loss of Correspondent Banking Relationships (CBRs)

Financial institutions involved in AML violations risk losing correspondent banking relationships, which are essential for international transactions, including trade finance and remittances. Loss of CBRs can isolate financial institutions and even entire countries from the global financial system, impairing economic growth and development.

The economic effects of AML crimes underscore the necessity for robust AML frameworks and international cooperation. Efforts to combat money laundering and associated crimes must be comprehensive, involving not only regulatory and law enforcement measures but also fostering transparency, good governance, and financial literacy. Mitigating the risks associated with AML crimes is essential for ensuring financial stability, promoting sustainable economic growth, and maintaining the integrity of global financial systems.

International Anti Money Laundering

International Anti-Money Laundering (AML) efforts play a pivotal role in combating financial crimes that transcend national borders. The global impact of AML measures and the role of international organisations are critical in establishing a unified front against money laundering and its associated crimes.

Global Impact of AML

AML measures have a profound global impact, enhancing the integrity and stability of financial systems worldwide. By curbing money laundering and terrorist financing, these measures protect economies from the disruptive effects of illicit financial flows, such as economic instability, loss of public trust in financial institutions, and reduced foreign direct investment. Effective AML frameworks also contribute to national security by obstructing the financial channels that support criminal and terrorist activities.

Role of International Organisations

1. Financial Action Task Force (FATF)

The FATF is the cornerstone of international AML efforts, setting the global standards for preventing money laundering and terrorist financing. It develops and promotes policies to combat these financial crimes, providing a framework for countries to implement effective AML/CFT (Combating the Financing of Terrorism) measures. The FATF’s recommendations are widely recognised as the international benchmark for AML/CFT efforts.

2. International Monetary Fund (IMF)

The IMF plays a crucial role in the global AML landscape by assessing the financial systems of its member countries for AML/CFT vulnerabilities. It provides technical assistance and training to help countries strengthen their financial sectors against money laundering and terrorist financing. The IMF also contributes to the development of international AML/CFT standards and collaborates with other organisations to promote global financial stability.

3. World Bank

The World Bank is instrumental in supporting countries in their efforts to implement effective AML/CFT measures. It offers technical assistance, policy advice, and capacity-building programs to help countries meet international AML standards. The World Bank’s involvement is crucial in ensuring that developing countries can effectively participate in the global fight against money laundering and terrorist financing.

4. United Nations (UN)

The UN, through its Office on Drugs and Crime (UNODC), plays a significant role in combating money laundering and related crimes. It offers legal and technical assistance to member states, facilitating the adoption and implementation of international treaties and standards related to AML/CFT. The UN also coordinates international efforts to fight corruption, drug trafficking, and other predicate offenses to money laundering.

Coordination and Standard Setting

1. Setting International AML/CFT Standards

The establishment of international AML/CFT standards is crucial for creating a consistent and effective global response to money laundering and terrorist financing. These standards ensure that all countries adhere to a minimum set of measures, facilitating cooperation and information exchange across borders.

2. Assessing Countries Against International Standards

International organisations regularly assess countries’ AML/CFT frameworks against established international standards. These assessments identify gaps and weaknesses in national systems, providing a basis for targeted assistance and reforms. They also promote accountability and transparency, encouraging countries to continuously improve their AML/CFT measures.

3. Capacity Development Delivery

Capacity development is essential for enabling countries, especially developing ones, to implement effective AML/CFT measures. International organisations deliver training, technical assistance, and policy advice to build the necessary institutional and legal frameworks. This support is tailored to the specific needs of each country, ensuring that AML/CFT measures are both effective and sustainable.

The global impact of AML and the role of international organisations are indispensable in the fight against money laundering and terrorist financing. Through coordination, standard-setting, and capacity development, these organisations foster a collaborative international environment that enhances the effectiveness of AML/CFT measures worldwide, ensuring a safer and more secure global financial system.

AML/CFT Policies in Practice

The implementation of Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) policies is a critical component in safeguarding global financial stability. The International Monetary Fund (IMF) plays a significant role in this regard, offering a multi-faceted approach that encompasses strategy development, surveillance, lending, capacity building, and policy advice.

AML/CFT Strategy (IMF)

The IMF’s AML/CFT strategy is designed to integrate AML/CFT measures into its broader financial surveillance and advisory functions. This strategy underscores the importance of effective AML/CFT frameworks in maintaining economic stability and preventing financial abuse that can undermine global economic growth. The IMF’s approach is comprehensive, addressing legal, institutional, and operational aspects of AML/CFT across its member countries.

IMF’s Role in Different Functions

1. Surveillance

The IMF conducts regular surveillance of its member countries’ economies, which includes assessing the robustness of their AML/CFT frameworks. This surveillance helps in identifying potential vulnerabilities in the financial system that could be exploited for money laundering or terrorist financing, thereby informing the IMF’s policy advice and capacity development efforts.

2. Lending

In its lending activities, the IMF considers the integrity and stability of a country’s financial sector, including its AML/CFT measures. Effective AML/CFT frameworks are seen as essential for ensuring that financial resources provided by the IMF are used for their intended purposes and do not fall prey to corruption or illicit use.

3. Capacity Development

The IMF provides targeted capacity development to help countries strengthen their AML/CFT frameworks. This includes technical assistance and training for financial sector regulators, law enforcement agencies, and other relevant bodies to enhance their ability to implement and enforce AML/CFT measures.

4. Policy Advice

The IMF offers policy advice to its member countries on how to improve their AML/CFT frameworks. This advice is based on international standards and best practices, tailored to the specific needs and circumstances of each country.

5. Financial Sector Assessment Programs (FSAPs)

FSAPs are a key tool used by the IMF to assess the resilience of a country’s financial sector. AML/CFT assessments are an integral part of FSAPs, evaluating the effectiveness of a country’s AML/CFT regime and its compliance with international standards.

6. Fund-Supported Programs

For countries receiving financial support from the IMF, AML/CFT measures are often incorporated into the program’s design. This ensures that financial systems are not only stable and efficient but also resistant to abuse by money launderers and terrorist financiers.

Policy Advice in Article IV Consultations

During its annual Article IV consultations with member countries, the IMF provides policy advice that includes AML/CFT considerations. These consultations offer an opportunity for a comprehensive review of a country’s economic policies and practices, including the effectiveness of its AML/CFT measures.

AML/CFT Capacity Development Program

1. Technical Assistance

The IMF’s technical assistance in AML/CFT focuses on building the institutional capacity of member countries. This includes legal and regulatory frameworks, financial intelligence units, and judicial and law enforcement capabilities.

2. Bilateral, Regional, and Thematic Assistance

The IMF’s AML/CFT assistance is delivered through bilateral engagements with individual countries, regional training centers, and thematic programs addressing specific AML/CFT challenges. This multifaceted approach allows for a more nuanced and effective capacity development.

3. Collaboration on Policy Dialogue and Analytical Work

The IMF collaborates with member countries and other international organisations on policy dialogue and analytical work related to AML/CFT. This collaboration enhances the understanding of AML/CFT issues, supports the development of effective policies, and promotes international best practices.

The IMF’s comprehensive approach to AML/CFT policies in practice underscores the importance of these measures in maintaining financial integrity and stability. Through strategic advice, capacity development, and a focus on integrating AML/CFT into broader financial sector assessments, the IMF plays a crucial role in enhancing the global financial system’s resilience to money laundering and terrorist financing risks.

AML Compliance Stages

AML (Anti-Money Laundering) compliance and regulations vary by country, but they share common elements that are recognised internationally. These elements form the backbone of efforts to prevent, detect, and deter money laundering and associated financial crimes.

Know Your Customer (KYC)

1. Customer Identification

Customer identification is a fundamental aspect of KYC regulations. Financial institutions are required to verify the identity of their customers using reliable, independent sources of documents, data, or information. This process helps in ensuring that banks and other financial entities know who they are dealing with, reducing the risk of money laundering.

2. Risk-Based Approach (RBA)

The Risk-Based Approach allows institutions to focus their resources on the areas of highest risk. This approach involves assessing the money laundering or terrorist financing risk associated with individual customers, products, and geographic locations to tailor due diligence procedures accordingly.

Reporting on Large Money Transactions

1. Currency Transaction Reports (CTR)

Countries often require financial institutions to file CTRs for transactions exceeding a specified threshold, typically involving large amounts of cash. These reports are critical for identifying patterns of activity that might suggest money laundering or other illicit financial activities.

Monitoring and Reporting of Suspicious Activities

1. Suspicious Activity Reports (SARs)

Financial institutions are obligated to monitor customer transactions for suspicious activity and report these to the relevant authorities without notifying the customer. SARs play a crucial role in identifying potential money laundering or terrorist financing operations.

Compliance with Sanctions Lists

1. Regulatory Bodies

Entities like the Office of Foreign Assets Control (OFAC) in the United States, the United Nations (UN), and the European Union (EU) maintain lists of sanctioned individuals, organisations, and countries. Financial institutions must screen transactions and relationships against these lists to ensure compliance and prevent inadvertently facilitating prohibited activities.

Consequences for Non-Compliance

1. Fines

Non-compliance with AML regulations can result in substantial fines for financial institutions. These fines are intended to serve as a deterrent and underscore the importance of robust AML compliance programs.

2. Regulatory Actions

Beyond fines, regulatory bodies can take a range of actions against non-compliant institutions, including license revocations, restrictions on business activities, and in severe cases, criminal charges against individuals involved.

3. Reputational Damage

The reputational impact of non-compliance can be significant and long-lasting. Financial institutions found lacking in their AML obligations may face a loss of confidence from customers, investors, and partners, potentially leading to a decline in business and market value.

AML compliance and regulations are designed to create a hostile environment for money launderers while promoting the integrity and stability of the global financial system. The effectiveness of these measures depends on the commitment of individual countries and institutions to implement and adhere to stringent AML standards and practices.

AML and Cryptocurrency

The integration of Anti-Money Laundering (AML) measures within the cryptocurrency sector presents unique challenges and opportunities. As cryptocurrencies gain widespread adoption, regulatory bodies and financial institutions are grappling with developing effective frameworks to mitigate the risks associated with these digital assets.

A. Challenges in Regulating Cryptocurrency

- Anonymity and Pseudonymity: Cryptocurrencies offer a level of anonymity since transactions can be conducted without revealing the true identity of the parties involved. This feature, while beneficial for privacy, poses significant challenges for AML compliance.

- Decentralisation: The decentralised nature of many cryptocurrencies means there is no central authority or intermediary that can monitor and report suspicious activities, complicating regulatory oversight.

- Cross-border Transactions: Cryptocurrencies can be transferred across borders effortlessly and instantly, making it difficult to apply jurisdiction-specific AML regulations.

- Lack of Uniform Regulation: The regulatory landscape for cryptocurrencies is fragmented, with different countries adopting varying approaches, leading to regulatory arbitrage.

B. AML Measures in the Cryptocurrency Industry

- Know Your Customer (KYC) Procedures: Exchanges and wallet providers are increasingly implementing KYC processes to verify the identity of their users, similar to traditional financial institutions.

- Transaction Monitoring: Continuous monitoring of cryptocurrency transactions to identify patterns that may indicate money laundering or other illicit activities.

- Travel Rule Compliance: Adhering to the ‘Travel Rule,’ which requires the originators and beneficiaries of cryptocurrency transfers to exchange identifying information, akin to traditional bank transfers.

C. Role of Blockchain Analysis and Monitoring Tools

Blockchain analysis tools play a crucial role in enhancing AML efforts within the cryptocurrency sector. These tools analyse blockchain data to track the flow of funds, identify high-risk wallets, and detect patterns indicative of illicit activities. They provide valuable intelligence for regulatory authorities and businesses to ensure compliance and prevent the misuse of cryptocurrencies.

D. Regulatory Developments in the Cryptocurrency Sector

- Global Standards: International bodies like the Financial Action Task Force (FATF) have issued guidelines for countries to regulate cryptocurrencies and virtual asset service providers (VASPs) under AML/CFT standards.

- National Regulations: Many countries have started to enact specific regulations for cryptocurrencies, defining the obligations of VASPs in terms of registration, licensing, reporting, and compliance with AML/CFT requirements.

- Collaborative Efforts: There is an increasing trend towards international collaboration and information sharing among regulatory authorities to address the global nature of cryptocurrency transactions and ensure effective oversight.

The cryptocurrency sector’s dynamic and innovative nature necessitates a flexible and informed regulatory approach. As the industry evolves, continuous dialogue between regulators, industry participants, and technology providers will be essential to develop effective AML frameworks that balance the need for financial integrity with the potential for innovation and privacy that cryptocurrencies offer.

AML Compliance and Regulations by Country

AML (Anti-Money Laundering) regulations vary by jurisdiction but share the common goal of preventing and combating money laundering and terrorist financing. Below is an overview of AML regulatory frameworks in the United States, European Union, and the United Kingdom, followed by a brief international comparison.

A. United States

1. Bank Secrecy Act (BSA): Enacted in 1970, the BSA sets the foundation for AML efforts in the U.S., requiring financial institutions to assist government agencies in detecting and preventing money laundering. Key provisions include record-keeping and reporting requirements, such as filing Currency Transaction Reports (CTRs) and Suspicious Activity Reports (SARs).

2. USA PATRIOT Act: Passed in response to the 9/11 attacks, this Act expanded the scope of the BSA to further prevent terrorist financing. It introduced measures like the Customer Identification Program (CIP) and enhanced due diligence for certain accounts, particularly those involving foreign individuals and entities.

3. Anti-Money Laundering Act of 2020: Part of the National Defense Authorisation Act, this Act is a significant overhaul aimed at strengthening the U.S. AML/CFT framework. It introduces, among other things, provisions for beneficial ownership reporting and expands the authority of the Financial Crimes Enforcement Network (FinCEN).

B. European Union

1. Anti-Money Laundering Directive (AMLD): The EU has issued several iterations of the AMLD, with the most recent being the 6th AMLD. These Directives set out the legal framework for EU member states to detect and prevent money laundering and terrorist financing, including KYC procedures, beneficial ownership registers, and enhanced due diligence measures.

2. European Banking Authority (EBA): The EBA plays a key role in standardising AML/CFT practices across the EU’s banking sector, issuing guidelines and recommendations to ensure consistent application of the AMLD provisions across member states.

C. United Kingdom

1. Proceeds of Crime Act 2002 (POCA): POCA provides the legal framework for recovering the proceeds of crime, including money laundering offenses. It includes provisions for confiscation, civil recovery, and cash seisure.

2. National Crime Agency (NCA): The NCA is responsible for combating serious and organised crime, including money laundering. It receives SARs from financial institutions and other entities.

3. Financial Conduct Authority (FCA): The FCA is the regulatory body overseeing financial services firms and markets in the UK, enforcing AML regulations among other responsibilities.

4. Her Majesty’s Treasury (HMT): HMT sets the UK’s financial sanctions regime and oversees the implementation of international sanctions, playing a crucial role in the AML framework.

1. Commonalities and Differences:

D. International Comparison of AML Regulations

- Commonalities: Most AML frameworks globally share common elements such as KYC requirements, the obligation to report suspicious transactions, the establishment of AML compliance programs, and adherence to international sanctions.

- Differences: Variations arise in the specifics of implementation, such as threshold amounts for reporting, the scope and detail of due diligence requirements, and the nature and severity of penalties for non-compliance. The approach to regulatory oversight and the specific agencies involved also differ across jurisdictions.

The effectiveness of AML regulations depends on robust national frameworks and international cooperation, given the global nature of financial crime. Despite differences in implementation, the overarching goal remains the same: to protect the integrity of the global financial system by preventing the flow of illicit funds.

Conclusion and Future Trends in AML

The ongoing significance of Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) cannot be overstated, as these efforts are crucial in safeguarding the integrity and stability of the global financial system. As we look to the future, several emerging trends and challenges, along with the evolving role of technology, will shape the AML/CFT landscape.

A. Ongoing Importance of AML/CFT

AML/CFT measures are fundamental in the fight against financial crimes, including money laundering and terrorist financing. These efforts not only protect financial institutions from being exploited for illicit purposes but also contribute to national and international security. The importance of robust AML/CFT frameworks continues to grow in response to the increasing sophistication of financial crimes and the globalisation of financial services.

B. Emerging Trends and Challenges in AML/CFT

- Cryptocurrencies and Digital Assets: The rise of cryptocurrencies and digital assets presents both opportunities and challenges for AML/CFT. While offering innovative financial solutions, they also create avenues for new forms of money laundering and financial crime that regulators are striving to address.

- Globalisation and Cross-Border Transactions: As financial services become increasingly globalised, monitoring and regulating cross-border transactions become more complex, requiring enhanced international cooperation and information sharing among regulatory bodies.

- Regulatory Divergence: The lack of uniformity in AML/CFT regulations across jurisdictions can lead to regulatory arbitrage, where entities engage in transactions in countries with less stringent regulations, complicating global AML/CFT efforts.

C. The Evolving Role of Technology in AML Compliance

- RegTech and Automation: Regulatory Technology (RegTech) solutions, including automation and machine learning, are transforming AML compliance by improving the efficiency and effectiveness of monitoring and reporting systems. These technologies can handle large volumes of transactions in real-time, identifying patterns and anomalies that may indicate illicit activity.

- Blockchain and Distributed Ledger Technology (DLT): Blockchain and DLT are being explored for their potential to enhance transparency and traceability in financial transactions, which could revolutionise AML/CFT practices by providing immutable records of transactions.

- Artificial Intelligence and Machine Learning: AI and machine learning are increasingly being deployed to analyse complex and large datasets, improving the identification of suspicious activities and reducing false positives, thereby making AML/CFT processes more intelligent and responsive.

Looking ahead, the AML/CFT landscape is set to evolve continually as new technologies emerge and financial criminals adapt their tactics. Staying ahead of these trends will require ongoing innovation, collaboration, and adaptation by regulatory bodies, financial institutions, and technology providers. The future of AML/CFT lies in leveraging technology to enhance regulatory compliance, improve operational efficiencies, and foster a more secure global financial environment.

What are the 5 pillars of compliance?

Essential Components of an Anti-Money Laundering (AML) Compliance Program

Pillar 1: Appointing a Compliance Officer

The foundation of an AML program is the appointment of a dedicated compliance officer. This individual is tasked with:

- Keeping Abreast of AML Regulations: Continuously updating knowledge on AML laws and changes in regulations.

- Communication and Implementation: Ensuring that all relevant stakeholders and management are informed about compliance requirements and updates.

- Audit Recommendations: Making informed suggestions based on compliance audits to enhance the AML framework.

- Staff Training Oversight: Managing the training of staff in AML compliance, ensuring they are well-versed in the latest practices and tools.

A profound understanding of AML legislation, coupled with comprehensive industry experience, is essential for this role, enabling the officer to navigate through various compliance scenarios effectively.

Pillar 2: Conducting Thorough Risk Assessments

Developing robust AML strategies involves:

- Creating Customised Solutions: Tailoring policies and controls to align with the unique operational risks of the institution.

- Management and Compliance Collaboration: Jointly identifying specific risks and formulating protective measures.

Pillar 3: Establishing AML Policies and Procedures Manual

A comprehensive manual for AML compliance is vital, ensuring:

- Employee Awareness: Every staff member is aware of how AML compliance impacts their role.

- Ongoing Training: Regular training programs keep employees updated on compliance tools and escalation procedures for suspicious activities.

Pillar 4: Continuous Monitoring and Maintenance

Maintaining the integrity of an AML program necessitates:

- External Audits: Regular audits by third parties focused on AML compliance, not just financial aspects.

- Frequency of Audits: Higher-risk institutions may require more frequent audits.

Pillar 5: Implementing Customer Due Diligence (CDD)

CDD is crucial for modern AML efforts, encompassing:

- Customer Identity Verification: Establishing customer identities and assessing their risk levels.

- Beneficial Ownership Identification: Uncovering true ownership to deter the use of shell corporations.

- Understanding Customer Relationships: Assessing how customer relationships influence risk.

- Ongoing Monitoring: Continual surveillance of transactions to identify unusual patterns or activities.

Implementing these pillars ensures a comprehensive and robust AML compliance framework, helping institutions effectively combat money laundering and financial crimes.

FAQs on AML

What is Money Laundering? Money laundering is the process of making large amounts of money generated by a criminal activity, such as drug trafficking or terrorist funding, appear to be earned legally. It typically involves three steps: placement, layering, and integration.

What is AML (Anti-Money Laundering)? AML refers to a set of laws, regulations, and procedures intended to prevent criminals from disguising illegally obtained funds as legitimate income. AML systems and controls aim to detect and report suspicious activities to the relevant authorities.

What is the difference between AML, KYC, and CFT? AML encompasses the broader framework and regulations aimed at preventing money laundering. KYC (Know Your Customer) is a component of AML that involves verifying the identity of clients. CFT (Combating the Financing of Terrorism) focuses on preventing funding to terrorist groups and is often integrated with AML strategies.

What is the AML compliance program in banking? An AML compliance program in banking is a set of policies, procedures, and technologies used by banks to comply with AML regulations, detect and report suspicious activities, and prevent money laundering.

What do you mean by anti-money laundering? Anti-money laundering refers to the measures and processes put in place to combat the laundering of money, ensuring that financial transactions are legitimate and not used to fund illicit activities.

What are the 3 stages of anti-money laundering? The three stages of anti-money laundering are:

- Placement: Introducing illegal funds into the financial system.

- Layering: Concealing the source of the funds through complex transactions.

- Integration: Reintegrating the laundered money into the economy as legitimate funds.

What is the AML KYC process? The AML KYC process involves identifying and verifying the identity of clients, assessing their risk profiles, and continuously monitoring their transactions for suspicious activities.

What is money laundering and examples? Money laundering involves disguising the origins of illegally obtained money. Examples include using cash businesses, smurfing (breaking up large transactions into smaller ones), and purchasing luxury items to sell later.

Who does AML apply to? AML applies to a wide range of entities, including banks, financial institutions, payment processors, real estate agencies, and other businesses involved in high-value transactions.

What is an example of anti-money laundering? An example of anti-money laundering is a bank detecting and reporting a series of transactions that appear to be structured to avoid reporting thresholds.

Who controls AML in the UK? In the UK, AML is regulated by several bodies, including the Financial Conduct Authority (FCA), National Crime Agency (NCA), and Her Majesty’s Revenue and Customs (HMRC), among others.

Why is AML important in banking? AML is crucial in banking to prevent financial crimes, maintain the integrity of the financial system, protect customer assets, and comply with legal obligations.

What is AML and CFT in banking? In banking, AML and CFT refer to the policies, procedures, and technologies used to prevent money laundering and the financing of terrorism, ensuring the bank’s services are not used for illicit purposes.

What is KYC sanction? KYC sanctions involve screening clients against sanctioned lists to ensure the bank does not facilitate transactions for individuals, entities, or countries subject to economic and trade sanctions.

Which is better AML or KYC? AML and KYC are not competing concepts; KYC is an essential part of AML efforts. Both are necessary for a comprehensive approach to preventing financial crimes.

What is KYC used for? KYC is used to verify the identity of clients, understand their financial dealings, and assess the risk they pose to the financial institution.

Also, Read about Risk-Based Approach (RBA) to AML & KYC risk management

About Neotas Due Diligence

Neotas Platform covers 600Bn+ archived web pages, 1.8Bn+ court records, 198M+ corporate records, global social media platforms, and 40,000+ Media sources from over 100 countries to help you build a comprehensive picture of the team. It’s a world-first, searching beyond Google. Neotas’ diligence uncovers illicit activities, reducing financial and reputational risk.

Due Diligence Solutions:

- Enhanced Due Diligence

- Management Due Diligence

- Customer Due Diligence

- Simplified Due Diligence

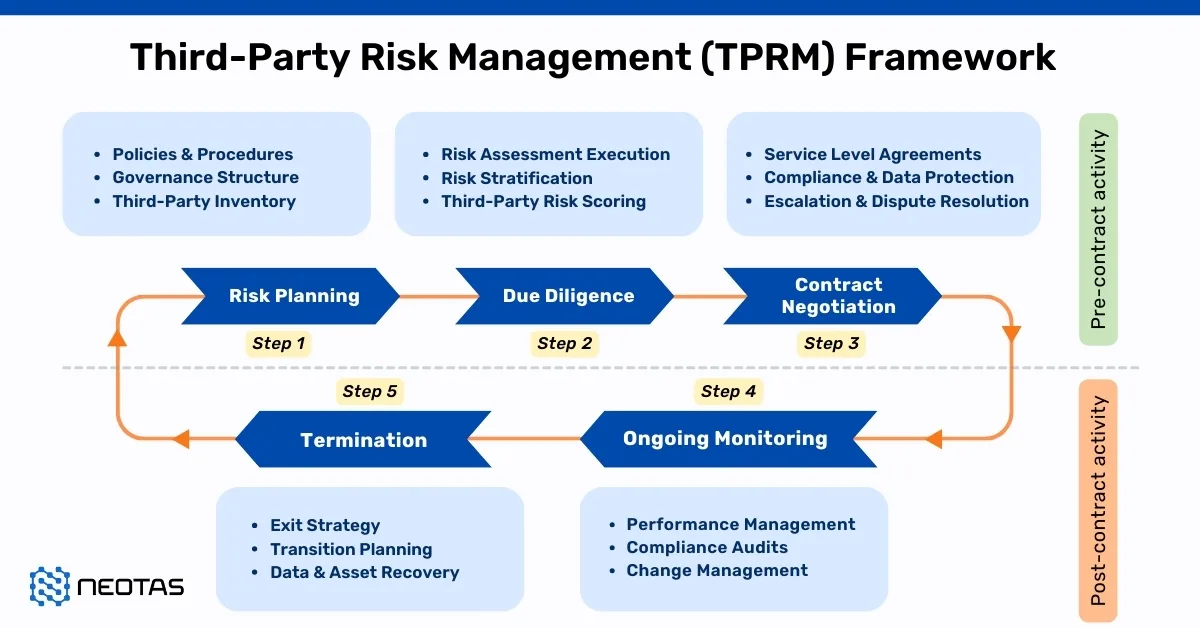

- Third Party Risk Management

- Open Source Intelligence (OSINT)

- Customer Due Diligence Requirements

- Risk-Based Approach (RBA) to AML & KYC risk management

- Anti-Money Laundering (AML) Compliance and Checks

- Introducing the Neotas Enhanced Due Diligence Platform

Due Diligence Case Studies:

- Case Study: OSINT for EDD & AML Compliance

- Overcoming EDD Challenges on High Risk Customers

- Neotas Open Source Intelligence (OSINT) based AML Solution sees beneath the surface

- ESG Risks Uncovered In Investigation For Global Private Equity Firm

- Management Due Diligence Reveals Abusive CEO

- Ongoing Monitoring Protects Credit Against Subsidiary Threat

- AML Compliance and Fraud Detection – How to Spot a Money Launderer and Prevent It

- What is Customer Due Diligence in Banking and Financial Services?