AML Compliance and Customer Due Diligence (CDD)

The 5th Pillar of AML Compliance – is there more data?

On May 11th, the four pillars of AML were joined by a 5th. The long-awaited legislation introduces the need to identify the beneficial ownership of legal entities for consumer due-diligence. As such, US financial institutions have introduced enhanced internal customer checks and additional measures to prevent criminals from using the financial system by proxy. Whilst the legislation aims to improve customer due diligence, underlying challenges remain.

These extra measures are conducted internally, allowing room for error that could prove costly to institutions. Rather than building a relationship with external partners, financial institutions are becoming reliant on potentially incomplete databases and are as such not objectively evaluating the report. Know Your Customer (KYC) policies are only useful if the data used to action them is valid and representative.

The use of open source intelligence (OSINT) can provide additional insight and reassurance for AML checks to prevent these expensive mistakes from happening, ensuring that you’re getting the whole picture. No doubt, the implementation of the 5th pillar brings benefits and is a step forward for KYC, but the question still remains: What more can be done? Why are the additional insights of open source intelligence not being used?

AML checks have advanced, yes. But used in isolation they only provide a part of the story. The use of OSINT alongside traditional AML checks provides enriched information that can be used to identify beneficial ownership. In addition, OSINT allows the information to be validated and checked externally, eliminating the risk of internal checks missing ownership issues that might prove costly in the future.

The influence of open sources can empower the 5th pillar by allowing external validation of ownership structures, thus providing much needed reassurance. The 5th pillar is a step in the right direction for financial institutions aware but the use of OSINT can strengthen its power.

Requirements of CDD

- Understanding Customer Relationships: Financial institutions are mandated to comprehend the nature and purpose of customer relationships to develop a comprehensive customer risk profile. This involves not only identifying the customer but also understanding the expected nature of transactions to detect anomalies effectively.

- Ongoing Monitoring: Institutions must conduct continuous monitoring of transactions to identify and report suspicious activities promptly. This ongoing scrutiny extends to updating customer information regularly, including beneficial ownership details for legal entity customers. Maintaining current and accurate data is critical for effective risk management.

- Risk-Based Approach: The CDD rule necessitates a risk-based approach wherein financial institutions evaluate customers and transactions based on the risk they pose. Higher-risk situations require enhanced due diligence measures. For instance, if a customer originates from a country known for high money laundering activity, additional checks, such as detailed source of funds verification and enhanced monitoring, may be warranted before account approval.

Significance of the CDD Pillar

The integration of the CDD pillar significantly enhances the AML framework in several ways:

- Enhanced Detection and Prevention: By thoroughly understanding customers and their transactional behaviours, financial institutions can better detect and prevent money laundering and other illicit activities.

- Regulatory Compliance: Implementing robust CDD processes helps financial institutions avoid hefty regulatory penalties and fines.

- Operational Efficiency: Maintaining accurate and updated customer information ensures that institutions can adapt quickly to evolving AML regulations and maintain operational agility.

Purpose of AML Compliance

AML compliance serves to protect financial institutions from being exploited for money laundering and other illicit activities. The primary objectives include:

- Customer Identification and Verification: Ensuring that the true identity of customers is verified to prevent the opening and use of anonymous accounts.

- Transaction Monitoring: Continuously monitoring transactions to detect and report suspicious activities.

- Risk Assessment and Mitigation: Evaluating and mitigating risks associated with money laundering and terrorist financing.

- Regulatory Compliance: Ensuring adherence to relevant laws and regulations to avoid penalties and reputational damage.

- Fraud Prevention: Protecting both the financial institution and its customers from fraud and financial crime.

An effective AML compliance programme is essential for maintaining the integrity of the financial system and sustaining public trust.

Key Components of an AML Compliance Programme

- Risk Assessment: Identifying and assessing money laundering risks associated with the institution’s products, services, customers, and geographic locations. Understanding these risks allows for the tailoring of the AML programme and efficient allocation of resources.

- Clear Policies and Procedures: Establishing clear, well-defined policies and procedures ensures consistent adherence to AML regulations. This includes mechanisms for front-office staff to report suspicious activities and ensure transaction integrity.

- Customer Due Diligence (CDD): Implementing comprehensive CDD processes, including verifying customer identities, understanding the purpose of their accounts, and assessing risk levels. Robust CDD involves collecting and verifying detailed customer information, screening against sanction lists, and continuous monitoring of customer activities.

- Suspicious Activity Reporting: Ensuring timely detection and reporting of suspicious transactions through a well-defined process for employees to report suspicious activities. Filing Suspicious Activity Reports (SARs) with regulatory authorities is a key component of this process.

- Ongoing Monitoring and Testing: Continuously monitoring transactions and account activities using sophisticated systems to identify unusual patterns and anomalies. Regular testing and independent audits are essential to assess the effectiveness of the AML programme and ensure compliance with evolving regulations.

- Know Your Customer (KYC) Programme: Implementing a rigorous KYC programme during customer onboarding and periodically reassessing customer risk profiles as new information becomes available. This involves gathering comprehensive data on customers, including their transaction patterns and geographical locations.

- Independent Audits: Conducting regular independent audits to evaluate the effectiveness of the AML compliance programme. These audits should be scheduled every 12-18 months, with more frequent audits for institutions operating in high-risk areas.

- AML Training: Providing regular AML training for all employees, with more specialised training for those with specific AML responsibilities. This ensures that staff are knowledgeable about AML procedures, regulations, and compliance requirements.

- Compliance Officer: Appointing a compliance officer with the requisite experience and knowledge to manage the AML compliance programme efficiently. This officer oversees the implementation of AML procedures and training.

Best Practices for Conducting AML Due Diligence

- Conduct Comprehensive Risk Assessments: Develop detailed risk profiles to identify potential money laundering risks. Regularly update these assessments to reflect changes in customer behaviours and external threats.

- Implement Robust CDD Procedures: Establish thorough procedures for verifying customer identities, assessing risks, and ensuring compliance with regulations. This includes screening against global sanction lists and politically exposed persons (PEP) databases.

- Utilise Advanced Transaction Monitoring Systems: Deploy sophisticated transaction monitoring systems that can continuously detect suspicious activities and transactions. These systems should be capable of learning and adapting to new money laundering typologies.

- Stay Updated with Regulatory Changes: Maintain a proactive approach to keeping abreast of the latest AML regulations and changes. Regularly update compliance programmes to reflect new regulatory requirements and guidance.

- Provide Regular Staff Training: Ensure that all employees receive comprehensive AML training to recognise red flags and conduct proper AML screening. Tailor training sessions to different roles within the organisation to enhance effectiveness.

- Conduct Regular Internal Reviews: Perform periodic internal reviews to assess the effectiveness of AML screening processes, identify areas for improvement, and address compliance gaps.

- Leverage Third-Party Solutions: Use competent third-party solutions to enhance AML screening accuracy and efficiency, reducing false positives and ensuring thorough coverage.

By adhering to these best practices, financial institutions can significantly enhance their AML due diligence processes, mitigate risks, and ensure compliance with AML regulations, thereby preventing money laundering and safeguarding their operations and customers from legal and financial repercussions.

Also, Read about Risk-Based Approach (RBA) to AML & KYC risk management

About Neotas Customer Due Diligence

Neotas Platform covers 600Bn+ archived web pages, 1.8Bn+ court records, 198M+ corporate records, global social media platforms, and 40,000+ Media sources from over 100 countries to help you build a comprehensive picture of the team. It’s a world-first, searching beyond Google.

Neotas’ diligence uncovers illicit activities, reducing financial and reputational risk. Enhance business risk assessment and mitigation with Neotas Customer Due Diligence.

Customer Due Diligence Solutions:

- Customer Due Diligence

- Enhanced Due Diligence

- Management Due Diligence

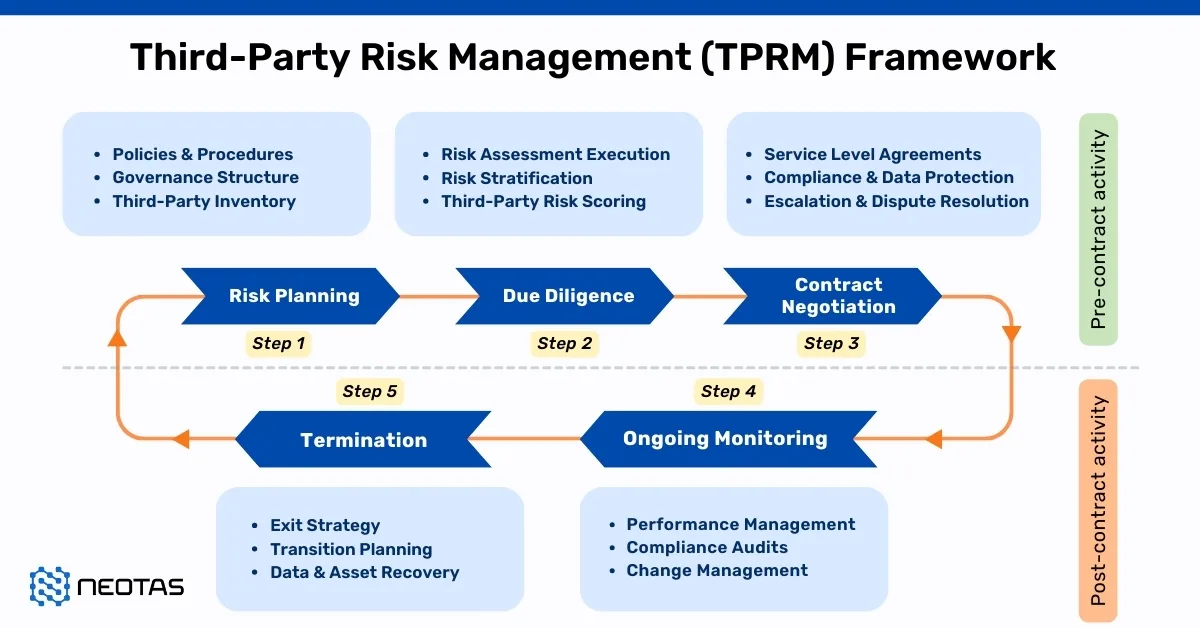

- Third Party Risk Management

- Open Source Intelligence (OSINT)

- Enhanced Due Diligence Checklist

- Customer Due Diligence Checklist

- Customer Due Diligence Requirements

- Introducing the Neotas Enhanced Due Diligence Platform

Case Studies:

- Case Study: OSINT for EDD & AML Compliance

- Overcoming EDD Challenges on High Risk Customers

- Neotas Open Source Intelligence (OSINT) based AML Solution sees beneath the surface

- ESG Risks Uncovered In Investigation For Global Private Equity Firm

- Management Due Diligence Reveals Abusive CEO

- Ongoing Monitoring Protects Credit Against Subsidiary Threat

- AML Compliance and Fraud Detection – How to Spot a Money Launderer and Prevent It

FAQs on AML compliance & CDD

What are the consequences of non-compliance with AML regulations?

Non-compliance with AML regulations can lead to severe penalties, including substantial fines, legal sanctions, loss of banking licenses, reputational damage, and reduced customer trust, ultimately impacting the institution’s operational viability.

How often should AML compliance programs be reviewed and updated?

AML compliance programs should be reviewed and updated at least annually. However, institutions operating in high-risk areas or experiencing significant regulatory changes may require more frequent assessments.

How do financial institutions ensure compliance with AML regulations?

Financial institutions ensure compliance by implementing robust AML programs, conducting regular risk assessments, maintaining accurate customer records, performing ongoing transaction monitoring, and adhering to regulatory reporting requirements.

How do financial institutions train their employees on AML compliance?

Financial institutions provide comprehensive AML training for all employees, with specialised training for those in high-risk roles, ensuring staff are well-versed in recognising red flags, reporting suspicious activities, and understanding regulatory requirements.

How do financial institutions monitor and detect suspicious activity?

Financial institutions use advanced transaction monitoring systems, conduct continuous surveillance of account activities, and employ data analytics to detect anomalies. Suspicious activities are investigated and reported to regulatory authorities promptly.

What are some common challenges in implementing AML compliance programs?

Common challenges include staying current with evolving regulations, integrating advanced technology, managing data accuracy, training employees effectively, and balancing regulatory compliance with operational efficiency.